In the Blind Spot (Swiss Banker Exodus, Gosbanking, Bunds)

This is a sneak giveaway of the Blind Spot Wrap for 25/03/23.

This edition of the Blind Spot Wrap was compiled by Izabella Kaminska and Dario Garcia Giner. If you like what you see, consider a subscription over on our home site the-blindspot.com. For a 20% discount promo code email me on izabella@the-blindspot.com saying you saw the offer on Substack.

Seizing the means of finance:

I argued that the period between the fall of Silicon Valley Bank and the fall of Credit Suisse amounted to 10 days that shook the financial world, a reference to the famous John Reed book that catalogued the Russian revolution and the seizing of the means of production.

I noted last weekend that I was embarrassingly wrong when I tweeted that the original Credit Suisse rescue package was an ingenious mechanism that could restore the common equity in the group and allow the bank to live another year. And I'm still a bit baffled by what happened.

In theory, buying your own senior debt back subpar with central bank money, and a note from the central bank that your capital and liquidity positions were within regulatory limits, and that both FINMA and the SNB were prepared to support you to the end, should have worked to revive equity in the group. But it didn't.

The impact on the senior debt of the opco instead looked like this:

I've since realised I had a big blind spot. I -- like a lot of people -- didn't know that the AT1 debt ranked below common equity and that the uncertainty over the pricing of these bonds was spooking the system. In practice what ended up happening is that the value extracted from senior bondholders didn't get transferred into the CET1 cushion to shore up the bank and limit the chances of triggering AT1 debt.

Instead, it de facto subordinated/clipped the senior debt with an early buyback in favour of transferring the value into a form of mutualised common equity at the SNB itself.

What do I mean by that?

Put simply, there is about a 50bn Swiss franc discrepancy in the accounting. Unlike the subprime crisis, which was all about asset deterioration and the need for write-downs on those assets, this crisis pertains to the opposite.

The assets are supposedly fine and likely to perform if held to maturity. It's just that there are not enough people out there prepared to fund them at that level in the interim period, other than the central bank. It's a quantum valuation situation.

If Credit Suisse really had the liquidity coverage ratio and tier 1 capital position the regulators claimed it did on March 15, then -- based on the equity value -- its book value was trading well below intrinsic market value. At a 3bn Swiss franc price tag, UBS acquired that book at a total steal. But it shouldn't be possible for assets to have two prices at the same time. The assets are either worth what the book value says they are worth, or they are not.

The UBS acquisition gave the book a live mark that implies the assets should be discounted by at least 50bn Swiss francs. Assets are assets. Credit Suisse may have had a stinking reputation but that should not have had a bearing on the liquidity it could raise by either repo-ing or selling its supposedly highly liquid assets.

This is what a bank balance sheet is supposed to look like:The whole point of holding High Quality Liquid Assets (HQLA) -- which are mostly government bonds -- is so that if there is a depositor run you can meet the liabilities by selling the liquid portfolio.

If your coverage ratio remains intact, as does your hypothetical capital tier 1 ratio on a risk-weighted basis, but the equity is vaporising, regardless -- this implies that what is really off is the accounting treatment of the HQLA assets.

The reason the accounting is off is because the capital requirements on a risk-weighted basis are not going up since the assumption remains that the HQLA are low risk. But what if the HQLA are not really HQLA because if they're all to be sold at the same time in a crisis -- especially in the context of large unmarked held-to-maturity valuations in the system -- the market won't be able to take it.

In that case, the bank is severely under-capitalised, relative to the amount of HQLA it holds, and exposed to significant asset concentration risk, engineered by the regulators themselves. On March 15, Credit Suisse was facing a scenario where its liabilities were contracting as people began pulling deposits, and had to be met with cash raised from its HQLA.

To keep everything in balance, the bank needed to prop up its capital or reduce its assets. If it sold the HQLA it risked materialising a loss that could expose that bank tier 1 ratios all over the system were off. The March 15 exercise wanted to avoid this by using an income trick, involving the closing out of wholesale funding liabilities below par, which would deliver an income that could magically bolster its HQLA.

In theory, this should have bolstered the common equity because -- if we continue to presume loan quality was never the issue -- once all depositor claims were met, fewer bondholders meant more cash leftover, distributable to the common equity tier. The fact that the equity tanked regardless, thus sent a much graver signal.

Either markets were behaving entirely irrationally (hence my blind spot) or what we were seeing was a collapse in confidence, not just in Credit Suisse, but also in the cash and HQLA component of its balance sheet.

The fact that equity value was retained post-collapse while wiping out the AT1 bondholders (probably to retain talent so as to ensure they can keep managing the derivative book) sent a further confusing signal. It signalled employees with deferred bonuses paid out in equity are a type of depositor who outrank bondholders, because chances are, by the end of trade, the main holders of Credit Suisse stock were the employees themselves.

It also sent a signal, I think, that this time round what went wrong wasn't really the fault of the employees or even the execs.

But what about the hedges? Wasn't Credit Suisse hedged?

Yes! Apparently so. And that's the irony. In theory, if CS had to materialise a loss on HQLA by selling it in the market it didn't matter. It was hedged. Any losses should have been compensated for by in-the-money returns from its hedges. But this could have opened the door to an even bigger problem: a large repricing of interest rate derivatives traded on centrally cleared exchanges, leading to an increase in variation margins and collateral requirements.

For those banks that aren't hedged - and there could be many - this would only increase the expense of doing so and make them even more exposed. It would also expose that, in the current market, the only way to square the mismatch without adding to inflationary pressure was by drawing losses from a counterpart who had sizeable cash buffers to draw on -- a counterpart such as the Saudis, who had now firmly signalled, in the case of Credit Suisse, they weren't prepared to take on any more losses.

Which brings us to the following pickle: To consolidate the Credit Suisse book into its own, UBS must mark any equivalent asset it holds at a price reflective of its own deal. Not doing so would be worse than poor risk management. But, if it does this, it faces the same problem as Credit Suisse, hence, we can assume, the need for a 100bn Swiss franc facility at the SNB for UBS to do the deal.

And now, another pickle. While markets may, at first, have responded positively to the news that liquidity was coming back in a big way to support these assets, they belatedly realised that, in the context of inflation, this was not good news. Expanded liquidity + inflation + central banks committed to continued rate-hiking is not the recipe for a healthy market.

All the more so now that the illusion tier 1 ratios count for anything outside of continued liquidity operations has been shattered.

In that context, it seems increasingly plausible that central banks are looking to CBDCs as mechanisms to control the money supply (and consumption) on a "meritocratic" basis (where the government decides the merit) in the face of such challenges. FYI - in mid-April I will be moderating a panel about the future of CBDCs in Switzerland at a Swiss embassy function with members of the SNB.

Deutsche Bank shares tanked on Friday as its CDS soared to new highs.

Once you understand the above, you understand that the issue isn't about the loan dynamics of any particular bank or even the culture. It's about the sensitivity of their regulator-imposed HQLA portfolios to rising interest rates. It shouldn't be a surprise as a result that the most exposed banks will be situated in countries that suffered the longest episode of negative rates.

All the other stuff only matters because banks that have already been significantly punished by the market for other things have significantly more exposure to risk-weighted HQLA and thinner capital layers. Deutsche has similar cultural issues to Credit Suisse, no doubt. But, potentially, it has an even bigger exposure to HQLA because the size of the bund market is so much bigger.

For over a year I've been warning the real risk is in the bund market. The potential unravelling of Deustche Bank, because of legacy bund portfolios, will make that clear. In such circumstances, the ECB will be forced to prop up the bund market, but it will be much harder this time because of the complexities of dealing with an imperfect fiscal union. - IK

The Swiss National Bank published its annual 2022 report.

The SNB’s latest annual report (2022) provides some indicators that hint the stress really began when the SNB pushed rates into positive territory last September. The report shows, for example, that, in order to push rates up, the SNB had to issue a large number of SNB bills into the market. But what it also shows is that the liquidity it mopped up with one hand it redistributed (about 100bn Swiss francs worth) back into the market with the other:

Also worth noting, eligible collateral increased from CHF157bn to 11.387 TRILLION in 2022:

UBS Group may use its takeover of Credit Suisse Group as an opportunity to rebuild its investment banking business in the Middle East.

According to Bloomberg, UBS wealth boss Iqbal Khan -- who was previously the bank's head of international wealth management -- is among senior bankers supporting the plan and is talking with private bankers from Dubai to Doha, as he tries to hang onto the stricken firm’s top talent.

It's worth keeping an eye on what happens with CS bonus pools, Michael Klein and the Middle East. I have a very strong suspicion (based on pure conjecture) that things in Swiss banking are not what they seem. The idea that some of this may have been self-orchestrated seems entirely possible to me. The Swiss private banking model has already taken a massive knock from Switzerland entering into information-sharing regimes with the EU and America. But it dies even more obviously under a full-reserve zero-privacy CBDC system.

When governments lose control of their territory, they sometimes move into exile. The most famous case of this is Taiwan. But what happens to bankers?

Consider how news that UBS and Credit Suisse were selling themselves to the Qataris and the Saudis outright, and relocating themselves to Dubai, would have gone down? It wouldn't. No such acquisition would have ever been approved, either, by ESG-minded shareholders, or, by the government.

But what's really in the worth of a bank? The talent. And the Trust.

And perhaps also the paid-in capital legacy wealth trapped in the equity price.

It's worth remembering that Iqbal Khan - now plotting the move to the Middle East - was at the heart of the Credit Suisse spying scandal that brought down Tidjane Thiam's reign. The fear at the time was that he was plotting to woo Credit Suisse staff over to UBS, and that this is what prompted the spying. - IK

The investigations editor at Prospect Magazine tweeted about the murky past of the other high-profile bank failure this month, Signature Bank, and its links to the Edmond Safra affair (and via that to the Russian financial crisis).

.In a submission to the Treasury Select Committee ahead of its inquiry into the rescue of the UK subsidiary of SVB next Tuesday, payments and banking consultant Bob Lyddon (who really does know his stuff) explained why, contrary to the government's claims, the deal does not bypass any taxpayer support.

The key issue is that it forces HSBC's supposedly UK ring-fenced balance sheet to absorb the hugely concentrated liabilities of SVB diluting its provisions for ordinary UK depositors. As Lyddon notes, the move was heavily influenced by intense government lobbying by fintechs and tech companies. Many of these companies benefit from government contracts or grants, or are co-invested in by the British Business Bank. Lyddon is especially scathing about fintech.

As he notes in the submission: "The sector has no revenue streams apart from deductions-from-face-value on card payments, which are taken from the sales proceeds of UK merchants and passed on to UK consumers in the form of higher prices, and from selling on customer data. The sector has acted as a propagator of Authorised Push Payment Fraud, amongst other forms of financial crime to which the recent ‘Dear Chief Executive Officer’ letter from the Financial Conduct Authority addressed itself. The letter indicates that the sector does not even keep its customers’ money safe. To create a nationwide playing field for it, however, UK consumers and business have had their access to cash and branch services truncated."

Around 2015, a time I was heavily focused on writing about fintech, I was asked to join a fintech venture capitalist firm in London. I declined the offer on the basis that I did not see any long-term viability in the sector. If banking is rentierism, fintech I concluded at the time, is merely distributed rentierism. - IK

Kyle Bass argued that Europe's "Milton Friedman moment" was upon it by flagging the below chart:

Just to spook markets further, the US Justice Department launched probes into Credit Suisse and UBS, amongst other banks, investigating whether financial professionals have helped Russian oligarchs evade sanctions.

Lots of notable hedge fund managers and billionaires made public calls for deposit insurance to be extended to the entire banking sector, among them Elon Musk and Bill Ackman. But more worryingly so did the Mid-Size Bank Coalition of America (MBCA) -- a coalition of US midsize banks.

Michael Howell of Cross Border Capita talked with Blockworks Macro and argued banks were facing a liquidity crisis, not a credit deterioration issue, and that we were possibly moving to a de facto nationalisation of the banking system. He afed that inflation wasn't going away and that Western central banks would have to initiate Yield Curve Control too.

When nations fail:

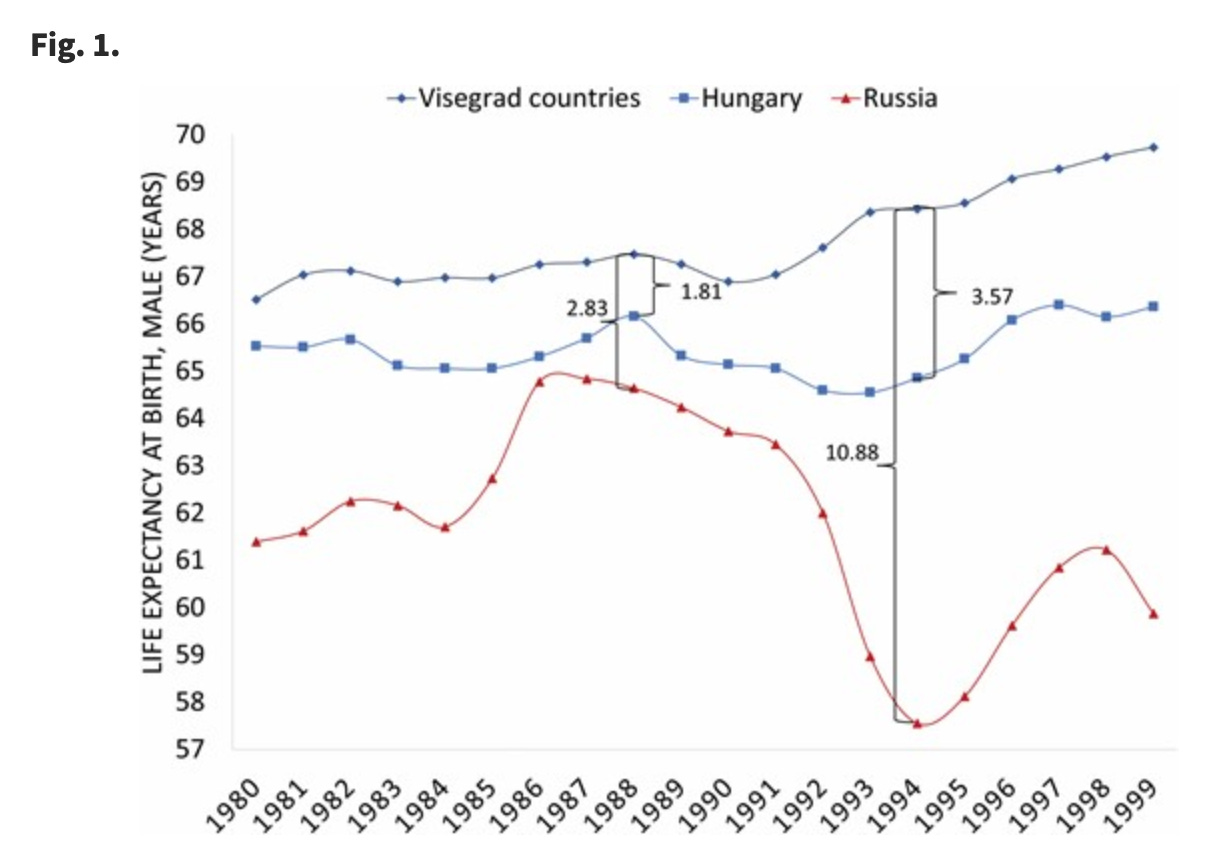

The Cambridge Journal of Economics published a very timely paper about the impact of deindustrialisation on mortality, following the collapse of the Soviet Union. It noted: "The results show that deindustrialisation was directly associated with male mortality and indirectly mediated by hazardous drinking as an stress-coping strategy."

It's worth considering whether some of these deaths might have been avoided, had the USSR anticipated the disaster and come up with a convincing narrative that allowed for an orderly (almost bank-like resolution minded) shift into a lower consumption model for its citizens. Had Russia's remaining wealth-generating resources been ring-fenced by the state, rather than them being plundered by foreign interests or domestic oligarchs, might the tragedy have been lessened? Or, for that matter, if the public had somehow been convinced that sacrificing consumption for the greater good was a virtuous act, and stepped up to do it voluntarily? - IK

Business, econ, finance etc:

The (potentially state-backed) Russian prankster duo known for duping European dignitaries into granting them interviews by pretending to be Ukrainian government officials, caught ECB President Christine Lagarde out by posing as Ukrainian Premier Volodymyr Zelensky.

In the call, Lagarde claimed the Russia sanctions had failed, and confirmed that during Poroshenko's premiership "strange characters" pocketed loans issued by the IMF. She also noted that CBDCs were needed to preserve Europe's sovereignty and prevent people from trading in other currencies.

The Swiss Finance Ministry halted the awarding of deferred bonuses for Credit Suisse bankers, leading to fears of a last-minute staff exodus in the troubled Swiss bank.

The problem is, if they quit - who manages the derivative book? There's a reason the US clung on to the British to administer the jurisdictions they formerly controlled after the British Empire gave way to Pax Americana.

Gold prices hit record highs in sterling terms, with international gold prices trading around $1,970.

.Eurodollar University's Jeffrey Snider (and friend of the Blind Spot) traced the history of our modern-day computer-powered financial plumbing infrastructure back to the 80s and explained how it impacts liquidity provision.

Snider agrees with the Blind Spot's assessment that intraday credit is being wrongly priced and that this is causing all sorts of problems. We will have more on this as soon as we have a chance to write it. - IK

Yannis Sournaras, Governor of the Bank of Greece, claimed that "Greek banks are solid", and their exposure to Credit Suisse is almost zero - stating "Greece is not Switzerland". He also cautioned against raising interest too quickly at the Politico Finance Summit in Paris last Thursday.

.Former Silicon Valley Bank employees blamed the bank's commitment to remote working for contributing to the bank's failure.

.Members of Jeffrey Gundlach's investment team met with a significant asset allocator prior to UBS' takeover of Credit Suisse. The asset allocator reported all their distressed debt managers thought CS bonds were 'money good' and would return par. They were off by 100 points. Oops..

.Investors were unnerved by dysfunctionalities in the currently 'wildly illiquid' bond market, as shown by the debacle of Credit Suisse's AT1 bond wipeout.

.Matthew Sedacca highlighted a study published by the Social Science Research Network, which recently found that nearly 200 more banks were vulnerable to the same risks that took down Silicon Valley Bank.

..A Twitter conversation exposed some of the secret sauce behind the Silicon Valley Bank banking model: skirting basic KYC protocols and US federal banking laws.

.Moody's warned that the rise in remote working had created a default risk for mortgage-backed securities due to record vacancy rates, which were causing record falls in US office space revenue.

.Walmart said it would close 12 stores across nine states and Washington DC this year, as they announced large layoffs at their fulfilment centres.

.Steven Englander at Standard Chartered highlighted the sudden disconnect between the 10-year US Treasury yield and the value of regional banks relative to the S&P 500:

Englander also highlighted that sterling had outperformed in FX compared to moves in rates over the last 10 days:

Central Bank watch:

Bank of England Governor Andrew Bailey resorted to Diocletian price edict inflation-fighting tactics by telling merchants not to raise prices because "if all prices try to beat inflation we will get higher inflation".

.

USD dollar liquidity swap line arrangements made a return, as announced by the Bank of Canada, the Bank of England, the European Central Bank, the Federal Reserve, and the Swiss National Bank, but the real action was in repos with the Fed's new FIMA facilities, which saw $60bn worth of liquidity drawn against collateral. The below is the comparative swap line usage:

The CEO of M-Pesa, the original revolutionary digital money payments system from Kenya -- which is owned by Vodafone vehicle Safaricom -- said the company would work hand-in-hand with the central bank of Kenya on a central bank digital currency.

M-Pesa is often presented by fintech cheerleaders as an example of the amazing things that can be achieved with private-sector digital payments solutions. Except, the main reason it came to dominate in Kenya is because the central bank was asleep at the wheel and didn't spot quickly enough that a private company was stealing its seigniorage power -- and by extension its monetary sovereignty -- by creating a monetary monopoly. M-Pesa executives will no doubt put on a brave face and argue their business model will not be threatened by the shift to a CBDC system, but I don't see how that is possible. This is the government claiming its monetary sovereignty back. - IK

Germany Watch:

Financial crisis expert Tuomas Malinen pointed out that there's a special facility in the Bundesbank which provides access to USD repo and suggested this implies that the massive withdraw could relate to Deutsche Bank. We’re double-checking that.

.Holger Zschaepitz of Germany's Welt pointed out that construction of new dwellings in Germany had collapsed. In January 2023, for instance, only 21,900 homes were permitted, a -26% YoY low since 2015.

.Bruce Packard reminded our Spot Markets Live chat about how German banking troubles could play into commercial real estate, flagging his old piece in MoneyWeek which had outlined the strange case of German property giant Adler's rapid rise and fall.

Too-big-to-fail tech:

Amazon fired an additional 9,000 workers in their Amazon Web Services, human resources, advertising, and Twitch live streaming groups. This comes as the group struggles to move group net income strongly back into positive territory.

Commodity corner:

Growth in the number of Chinese flights (up by an estimated 168% y/y) contributed to a record number of Chinese purchases of certain crude grades, taking advantage of low oil prices

Pierre’s Andurand’s oil hedge fund slumped by 40 per cent.

Farmers' political power:

The Dutch farmer's citizens movement gained so many seats in the Dutch Senate that the ruling coalition, composed of several centre and right-wing parties, will not be able to form a majority - even with the help of the Green party and Labour.

While European elites may look in fear at the disaster seemingly created by Mark Rutte's harsh anti-nitrogen Dutch farming reform, the Dutch premier may have less of the blame to share.

Observing videos shared by the Dutch farmers online, especially during the wild Dutch farmers' protests' zenith in 2020-2021, it's clear the farmers considered their opposition to be international.

Dutch farmers may have protested directly against the Dutch farming reforms, but the videos are loaded with the same alt narrative we've all come to know and love; a fight against a shady, anti-cash, liberal elite that supposedly organise in the World Economic Forum.

What this seems to suggest is that the electoral force behind the Dutch farmers party is a pan-European -- and potentially pan-Western -- phenomenon. This mangled coalition of different urban and rural interests, of traditionally different left and right-wing cleavages, could be copy-pasted anywhere else.

And that perhaps, several hundred years after the Netherlands reared its head as a leader in trade in the European continent, the Dutch are leading the way in political innovation once again. - DGG

You're either in power or in prison:

Arizona's Supreme Court declined most of Kari Lake's appeal, which challenged her defeat in the governor's race. However, the court stated the former Republican candidate for Governor was correct in claiming a lower court had erroneously dismissed her claim challenging the application of signature verification procedures on early ballots in Maricopa County.

.According to "off narrative" sources, documents obtained by the House GOP seemed to prove that CCP money has flowed to the Biden family. Jesse B Watters of Fox News also spoke on how China funnelled $35k to Hallie Biden, as Hunter Biden admitted he accepted money from Chinese figures.

.The New York Post revealed that Hunter Biden had a mole in the FBI nicknamed "One-Eye" who would tip off his Chinese business partners if they were under investigation by the United States.

.Trump claimed he would be arrested this Thursday, but it never happened. In the interim, the world learned about how scarily convincing deepfake news photos are these days.

Was that the true purpose of the misdirection? To seed doubt in the minds of people when something truly unbelievable happens for real?

Midjourney, the world's foremost AI painting software, appeared unable to generate images of Xi Jinping. A Twitter user shared images of Midjourney's AI depicting a Chinese invasion of New York, though the AI labeled the users' request to include Jinping as a "banned prompt".

.Emmanuel Macron performed an amazing disappearing luxury watch trick live on TV while defending his government's decision to move the retirement age from 62 to 64 amid mass protests in France.

When your business model is informing to the Feds:

Riccardo Spagni, founder and lead maintainer of privacy coin Monero, was gripped by rumours that he was working with Interpol.

TikTok tactics:

The recent rush of measures by the American and British governments to restrict the use of TikTok amongst federal or government employees may lead to the general banning of the popular Chinese social media app. The New York Times revealed that TikTok officials have put a plan in place to combat such a ban with Project Texas, a plan which would spin off TikTok's US activities into a US-based subsidiary. TikTok said they believed this subsidiary, run by an independent board of directors and not subject to ByteDance, would help to alleviate Western concerns regarding the app.

Politico's finest:

The collapse of Silicon Valley Bank and Credit Suisse shone a light on the failure of Western regulators to reform the banking sector following the massive taxpayer-funded bailouts of 2008.

.New York neared a deal to ban gas stoves in new homes.

.An investigation exposed that Russian oil has an open back door into Europe. A series of middlemen have been re-routing Russian oil through different neutral jurisdictions until it is sold in Europe without the Russian label, politicians and industry insiders claim.

The Blind Spot has drawn attention to the issue of Russian sanctions avoidance on several occasions, notably in this piece.

We can also report that following conversations with a would-be trader in sanctioned Russian oil, the Russian oil is being sold in Kazakhstan by middle-men. Sometimes, the corporations registered for these purposes in the Caspian country are actually incorporated in Western nations like Canada.

Once sold, the oil is stamped as 'Kazakh' and shipped to Bahrain or Qatar, where it is re-stamped as Bahraini or Qatari oil.

From there, the oil can enter European ports without a discounted pricetag, enabling middlemen to walk away with large amounts of cash for their troubles. - DGG

The city of Antwerp analysed water from the city's toilets and discovered their citizens' average daily use of cocaine has doubled since 2020.

.Xi Jinping's three-day visit to Moscow showed deepening ties between the two countries. Isolated from Europe, the visit highlighted Moscow's necessary reliance on its new Eastern partner for commodity and energy exports.

Since the surprising deal between Iran and Saudi Arabia was brokered on March 10 by China, we've watching Xi Jinping's moves for indications of further peace-inducing dealmaking. Recent revelations from the Japan Times show that Washington is aware that a war-weary world may embrace a China-brokered peace plan for Ukraine.

We wonder what, beyond commodity and energy exports, may have been agreed to between the two leaders. Most Western media have mockingly focused on Russia's new standing as a junior partner to China. And developments following the summit bear this out: reports show Xi Jinping immediately organised a meeting of former Soviet Central Asian countries, Russia's geopolitical back yard, for the first China-Central Asia summit on Wednesday.

But, especially as time goes on, it makes little sense to frame the entire deal as a 'lol Russia loses' story.

We are talking about an alliance between two quasi-despotic, manpower-rich countries whose economies suit each other like a yin and yan. One energy and mineral rich nation with a beleaguered industrial regime, the other industrially rich but energy deficient. If the pipes can be made to flow in the right direction, there's a major power forging recipe at hand.

It is easier to mock Russia than wake up to the Western alliance's stagnation. Just see this eery conversation between Xi Jinping and Putin. - DGG

Saudi Arabia said it would restore ties with Syria, as part of the Iran-Saudi cooldown mediated by China.

Geopolitical Hot Spots:

Seymour Hersh's latest article expanded on his breakthrough investigation, which claimed the Biden administration had personally ordered the destruction of the Nord Stream pipelines. In this piece, Hersh focused on how the German and American administrations could be establishing a plausible 'counter-narrative' for the German and American presses.

.Elisabeth Braw wrote on why insurers and companies worldwide were itching to find out who blew up NordStream for Foreign Policy. Braw claimed that if the explosion were deemed a state action, it could count as an act of war - meaning the explosion would not be covered by regular insurance.

.Rand Paul asked in Tweet whether Congress should have a larger say on America's overseas engagements, as opposed to the increasing tendency of the American executive to decide such matters unilaterally. Elon Musk tweeted back, "the forever war" - a subtle reference to the dystopic future predicted by George Orwell in which a perpetual war is waged between three great continents, mostly to keep the population pacified, controlled and impoverished.

.A reminder that the wife of former Cabinet Minister Jeremy Hunt once presented a TV show on Chinese state-run media. The show was accused of 'whitewashing' human rights abuses by the Chinese Communist Party.

.Xiao Qian, Ambassador of the CCP to Australia, claimed that, while the invasion of Australia is a fallacy, "Taiwan will be ours".

.Amidst deteriorating U.S.-Mexican relations, Mexico's president Lopez Obrador made a number of direct claims regarding the United States. Notably, he asked his audience: "Why are one or several cartels allowed to freely distribute fentanyl within American borders?".

Dystopic times:

Margot Cleveland wrote a piece for the Federalist that found American tax dollars were funding the development of AI and machine learning technology that "will allow the government to easily discover "problematic" speech and track Americans reading or partaking in such conversations."

One can quickly slip into dystopian practices when monitoring "problematic" speech.

While at Kroll, one of our projects was vetting influencers for beauty brands. One of these influencers passed with flying colours, only for them to be outed as the creator of a notorious QAnon blog some weeks after our report was submitted.

To stop such a mistake from happening again, I started delving into the fascinating world of natural language processing and machine learning algorithms.

Software like LIWC seemed to hold great promise; establish a 'fingerprint' of any influencer you want based on their particular typing characteristics, and use this 'fingerprint' to match to anonymous writings on notorious blogsites.

My excitement at being involved in such a groundbreaking project quickly led to fear. I found the organisation we were to partner with had recently pitched their new software to the Canadian government. They proudly boasted this tool could identify 'anti-vaxxers' based on their Twitter and social media posts. The tool didn't even need the 'anti-vaxxer' to post anything negative about vaccines! - DGG

Matt Taibbi shared a piece by Graphika, explaining why the idea that elites consider people too silly to digest news without guidance by strong authoritative figures means "anti-disinfo efforts focus not on telling the truth, but eliminating scepticism and enhancing authority." Taibbi's thread expands on how the technique works.

This is, as far as I can see, a mechanism that draws on gaslighting techniques and shaming those who don't agree with you, rather than appealing to their logic with superior reasoning that supports your standpoint. - IK

Vatican intrigue:

Pope Francis offered a lengthy interview on the subject of Latin American politics, and the topic of Catholic policies regarding sex in which he argued that Pope Gregory VII's 884-year-old decree on priestly celibacy was a 'transitory' ruling, and should not be considered eternal.